DEEP DIVE: Is voting rational? In swing states, YES

Correct votes have a shockingly high value in swing states

The conventional wisdom is “everyone should vote. Do your civic duty!” But I’m in enough contrarian circles that I also hear “I don’t vote, because voting is irrational. A single vote never determines an election.”

Are the critics right?

Before researching this post, I assumed that they were right about a single vote being irrelevant for Presidential elections. However, I still thought voting could be justified on “cultural/collective-action” grounds: Sure, your one vote will never matter, but if smart/ethical/pro-freedom people create a general cultural norm of voting, that can be enough to sway elections.

I’ve now gone through the literature on this subject. It turns out that, when one correctly calculates the chances of one vote flipping an election, one gets very high dollar values for a single vote.

Specifically, I estimate that a single correct vote for President in any of the seven key swing states is worth $10,000 or more, using low-end estimates. A correct vote in semi-competitive states is worth between $500 and $10,000 (that category includes states like Florida, Texas, Alaska, Minnesota, New Mexico, and New Hampshire.) It’s only “irrational” to vote for President in true blue/red states like Illinois or Wyoming, where the outcome is essentially certain.

Below, I explain in detail how I got those estimates.

How likely is a single vote to flip an election?

I enjoyed diving through the academic literature on this.

Zach Barnett, an Assistant Professor of Philosophy at Notre Dame, has a paper showing that previous research on the issue used the wrong statistical distributions in estimating the chances of a vote tipping an election.

Barnett’s logic for his calculation method is elegant and clear, and he illustrates it with a hypothetical election between “Donald” and “Daisy” that has exactly 1,000,001 voters. He lists all the possible vote combinations:

1-in-a-million is the hard, proven, lower bound. But we also know that vote combinations in the middle of the distribution are dramatically more likely than at the edges.

Barnett goes on to show that the chance of a single vote flipping an election is at least 5x higher for the most competitive races (below, “d” means the chance your vote in decisive, and “N” means the number of voters):

So what does “4 / N”, etc, mean in the real world? Let’s zoom in on Pennsylvania, often the most swing of all swing states. Currently, Kamala Harris has a 40% chance there:

In Pennsylvania in 2020, there were 6,840,276 people who voted for Trump or Biden. If the same number of people vote this year, then the chance that one additional vote in the state will determine the election is at least 4/N, or 4/6,840,276.

Simplifying, the chance is 1 in 1,710,069.

So we get a real-world lower-bound estimate that a single vote in Pennsylvania has roughly a 1-in-2-million chance of determining the President.1 If the Pennsylvania race tightens again to being 50%-50%, then it will be closer to 1-in-a-million.

In other words, if you vote in Pennsylvania, you’re essentially buying a lottery ticket that you’ll get to decide the election. Your odds are actually a lot better than for winning the popular “Mega Millions” lottery (1-in-300-million.)

That result is also plausible looking at history. While a 1-in-2-million chance has not yet occurred in the short history of American Presidential elections, when surveying America’s tens of thousands of local elections, we DO see plenty of races being decided by a coin toss or drawing lots from a hat due to being an exact tie, where a single vote would have been determinative. There are tens of thousands of local races in a major election year, and local races often have tens of thousands of voters, so consider that some real-world confirmation of Barnett’s math proofs.

How valuable is an election outcome?

In order to estimate the value of a vote, we need to have a sense of the value of an election.

There are no academic estimates on that.2 People who have written on this instead use guesstimates. Philosopher Will MacAskill guessed it this way in 2015 (in the following quote, I’ve updated his numbers for 2024): “total spending of the US government is $3.5 $6.1 trillion per year … if that money is spent 2.5 percent more effectively, then the benefits amount to $1,000 $1,753 per person… $314 $547 billion…”

Guessing is a better approach than having no estimate at all, but, below, I’ll look at stock market changes to get some empirically-grounded sense of how much a vote could be worth.

My approach below was to estimate the societal value of electing the better President by examining the absolute change in the stock market (S&P 500) on the day following Presidential elections, going back twenty years to 2004.

Here’s the change the day after election day, for each election:

We could refine those estimates a bit. The refinements don’t make a difference to the general magnitude of the value of a vote, so I won’t bore you with the details, except in a footnote.3 But basically, I do two things: I remove the median daily stock swing, and adjust for how much prediction markets had already priced in candidates’ wins.

The chart of whether markets already expected wins is interesting in its own right:

After adjusting for that, the median change was from the 2020 election, where Biden’s 20% increase in odds from election night appeared to be worth about 1.71% of the stock market, indicating that his election as a whole was worth about 6.57%.

The lowest-impact election was 2016, in which Trump’s win over Clinton was valued at 1.39% of the market.

So that suggests that the value of a vote ranges from 1.39% to 6.57% of the S&P 500.

In 2024, with the S&P worth $55 trillion, that works out to $767 billion – 3.61 trillion.

There are lots of reasons why my measure is imperfect. The goal isn’t to get a perfect measurement, it’s to get a number that’s in the right order of magnitude. If it’s more sound than MacAskill’s guess, then we’re making progress. In fact, my lower-bound estimate turned out to be not that far from his guess (though I looked his up afterward doing the calculations.)

One further issue is that we’re looking at the change in the stock markets caused by all elections on election day, including House/Senate/Governors, etc.

It turns out that total donations to Presidents are only a quarter of all donations to federal candidates, and only 23.67% if one also considers spending on governor’s races.4

So let’s estimate that the Presidency is worth 23.67% of all elections on election day (that feels low, but that’s what donation stats suggest, and they’re a “market” in a sense.) Then our new estimated range for the Presidential election goes down to $182 billion - $852 billion.

That estimate feels low. It amounts to about a mere 3% to 15% of one year of government spending. It’s just 0.7% – 3.4% of one year’s economic output.

It seems especially low when one considers that any effects of Presidential policy are compounding, and continue far into the future. For example, the 2017 Trump tax cuts still impact the economy 7 years later. Obamacare still affects us 15 years after enactment.

The stock market does include those indefinite effects (with discounting) in its $182 billion - $852 billion implicit estimate.

I should note that social issues and foreign policy may each be just as important as economic policy, but they can’t be quantified here. So this is, in every sense, a lower-bound estimate on the value of an election.

But at least we now have a ballpark number for that.

Let’s now see what happens when we combine it with the 1-in-2-million odds we calculated earlier.

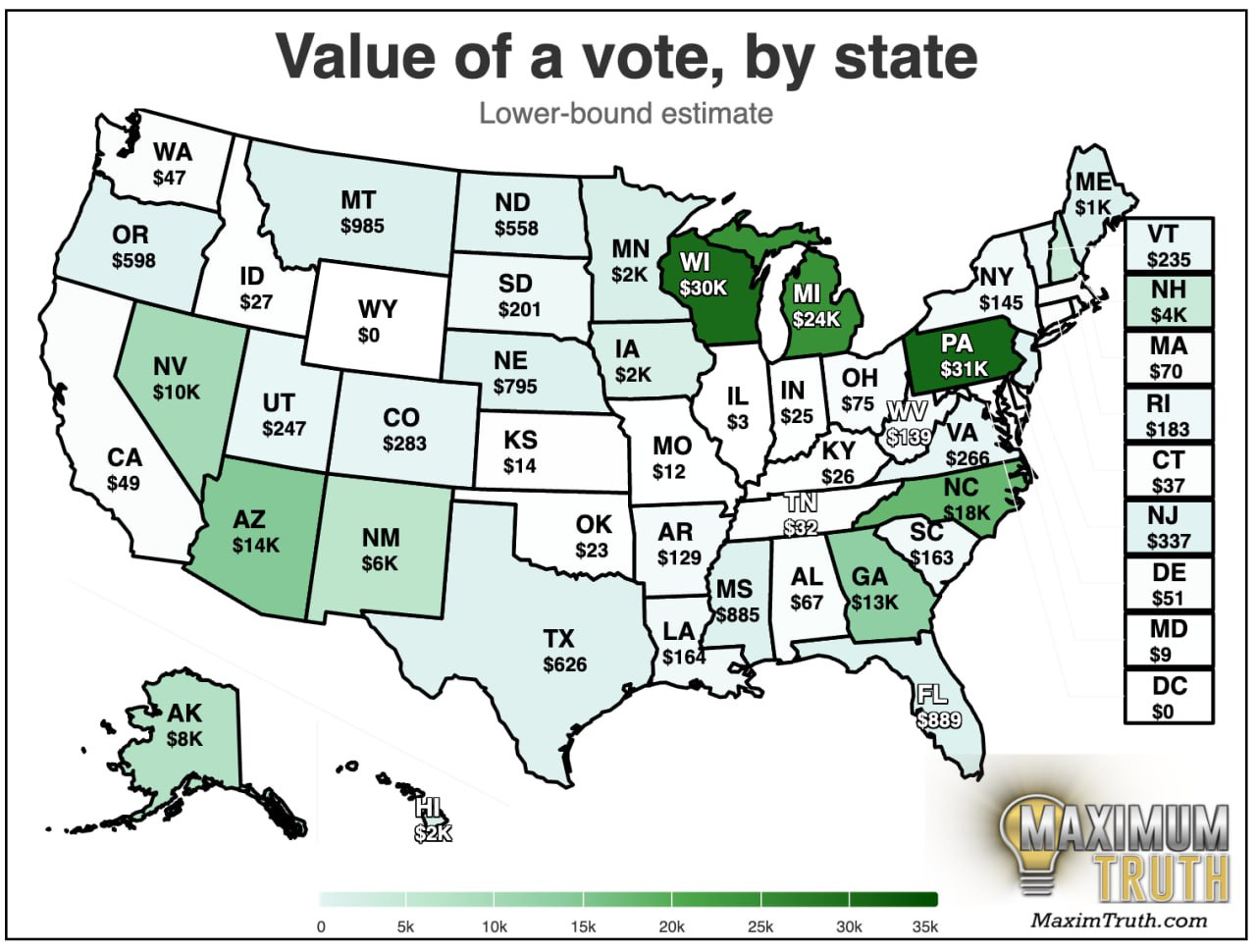

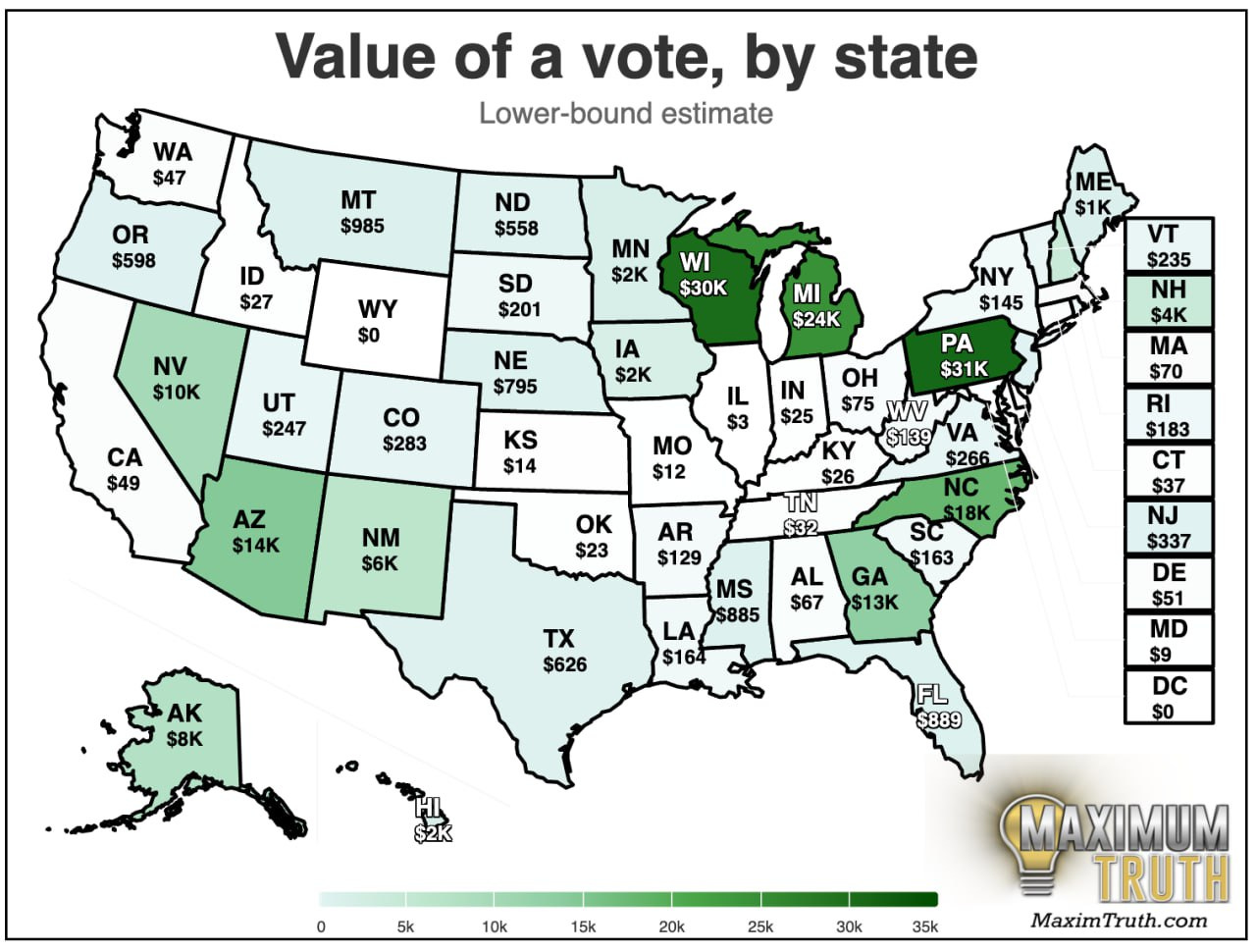

The Enormous Value of A Correct Vote in a Swing State

First, we’ll take Nate Silver’s model’s estimate (paywalled)5 that Pennsylvania has a 29% chance of tipping an election. Then, the expected value of your vote is:

[Chance of state determining Presidential election] * [Chance of voter determining state] * [Value of best candidate winning]

So:

Low-bound estimate: .29 * (1 / 1,710,069) * $182 billion

Higher estimate: .29 * (1 / 1,710,069) * $852 billion

Doing the math:

Low estimate: $30,864

High estimate: $144,485

Wow! The first time I crunched those numbers, I was shocked. $30k per vote, as the low-bound?

But I keep checking over the math, and it appears to be right. Also, while this estimate is empirically-backed, if you prefer any other plausible guesstimate about the value of electing the better President — you’ll still get massive values.

Looking beyond Pennsylvania, here are the other states:

There is, however, one possible factor we haven’t included yet:

Problem: You don’t know who the better candidate is!

The above assumes that you, as a voter, know which candidate would be better for the country.

However, as philosopher Jason Brennan points out in this paper (paywalled), if you vote for the wrong candidate, you cost society the same amount of money. Brennan notes:

“Remember: if a vote [for the right candidate] is like donating $3,000 to a charity, a vote the other way is like destroying $3,000 of their funds.”

So let’s say you’re barely better than the median voter at selecting the right candidate. Let’s say you’re only 60% sure that you picked the better one.

Then the value of your vote in Pennsylvania would shrink to: (60% - 40% = 20%) of the original estimate.

So if we assume you should only be 60% confident in your vote, then a Pennsylvania vote is actually worth $6,173 to $28,897 (instead of $30,864 to $144,485.)

That’s still worth a lot. Even you’re deeply conflicted, but have a gut sense who will be better for the country (60% sure) it’s still well worth your time to vote.

Here’s how the map changes, with that assumption:

Now, most of us are more than 60% sure. Maybe we’re 95%, or 100% sure. But should we be that sure?

History gives us lots of room for humility.

Why we should be humble about whether we know which candidate would be best

The famous biography of Sam Bankman-Fried, “Going Infinite”, documents how, when Bankman-Fried was a trader at Jane Street in 2016, he brilliantly modeled the election night results, and called Trump’s win before anyone else. He then used that information to short-sell the stock market, as he assumed that a Trump win would be bad for markets.

Markets instead rose the morning after Trump’s win, causing Bankman-Fried’s employer to have one of its largest single-day losses in its history, according to the book. Bankman-Fried had been overconfident about the market’s view of whether Trump was the better candidate.

It might feel “obvious” that smart people are better at voting, but some studies have shown that when it comes to political bias, smart people may actually better at fooling themselves and confirming their biases. Jason Brennan cites a paper by Dan Kahan, which provides some low-confidence evidence that smart people are more willing to let a negative view of their political opponents impact their views, when it comes to politics.6

There are also some real-world examples that should give us pause.

For example, California voters support green energy, and so they elected active politicians who imposed mandates, gas taxes, and subsidies, to guide the economy in that direction. In contrast, Texas voters don’t care much about “green” energy, so they elected politicians who mostly sat back and didn’t do much. The result:

The trend is not because Texas has more sunshine; it doesn’t.

California has somewhat more highly-educated voters than Texas does, but they may have tripped themselves up by thinking that they could plan their economy.

So many things are also just hard to predict. For example, nobody remembers that George W. Bush ran in 2000 as a dovish non-interventionist! He then invaded Iraq, with disastrous consequences.

Unpredictability even goes beyond a President promising one thing and doing another. You have backlash and “game theory” effects. For example, most Democrats were happy when Obama won re-election in 2012 – but Brennan points out that it set the stage for Trump’s victory in 2016. If one believes Democratic rhetoric about Trump being an “existential threat” to democracy itself, then, Brennan notes, in retrospect Democrats should wish they had voted for moderate Romney in 2012, just to preclude a Trump rise.

With all this, by far the best argument against voting, even in a swing state, is that you’re no better than the median voter at picking a candidate.

But how often have you heard someone give that reason for not voting?

You are much better than the median voter

Notwithstanding the above, I strongly suspect that the readers of this blog (and “rationalists” generally) are better able to pick Presidents than the median voter.

That’s because a relatively high proportion of this blog’s readers: A) tolerate hearing views they disagree with B) at least try to put aside biases when deciding things C) have heard of prediction markets and other ways of reducing bias.

Speaking of which, Brennan invokes prediction markets as an thought experiment for why you shouldn’t vote. Here’s his logic: “If you are not able to get rich from such markets, then you have evidence that you are not a reliable predictor when it comes to politics.”

But Brennan sets much too high a bar, because it’s possible for someone to be an amazing predictor compared to the median voter, and also lose money vs the wisdom of the market consensus.7

The real test should be: Let’s give you, and the median voter, each $1,000 to make bets about politics and policy with each other (not with the market.) Who ends up with more money in the end? If it’d be you, then you should vote.

My strong bet is that the majority of readers of this blog would significantly outperform the median voter on that correct test.

To be clear: Voting is not narrowly, selfishly, rational

Voting is a “social good.” As shown above, the benefit of picking the right candidate to lead the most powerful country in the world is enormous.

But the benefit to any given voter from his/her own vote is still small.

For example, let’s take our low-end estimate that picking the best candidate is worth $182 billion to the country as a whole.

$182 billion divided by the US population of 333 million is a $546 gain per American. Not nothing.

But now combine that with the fact that, even in Pennsylvania, your odds of deciding the election are 1-in-2-million.

That means the expected value of your vote for yourself is approximately ($1,153 / 1 million), or about one 32nd of a cent.

So it’s indeed not (narrowly, selfishly) rational to vote.

Now, we’re all somewhat selfish. But unless you’re a sociopath, you care at least somewhat about broader society doing well, too.

Conclusion – vote, if you live in a swing state

The above suggests that there are three things that justify voting:

You live in a somewhat competitive state

You try to be unbiased and informed

You want to improve society

If you check those boxes, and could out-bet the median voter, then I hope you’ll vote (regardless of whom you pick.)

Speaking of which, who do you pick? This is a survey just for readers who managed to read the full article!

If you liked this post, please consider sharing it, hitting the “heart” to like it (the helps the algorithm show it to more people) and subscribing!

Now, is that plausible? At first I thought it must be wrong, because – wouldn’t a “1 in a million” chance for your vote suggest that multiple voters tip the election every year? But the answer is that it makes sense because, when there is a decisive vote, EVERY voter on one side becomes decisive. To take a concrete example: Let's say that Pennsylvania is decided by a single vote. In that case, 3 million (plus 1) Pennsylvania voters will have been decisive.

“After doing an extensive search … no high-quality journal has published an estimate of net welfare effects of an entire presidency or congressional tenure.” — paper by Jason Brennan, 2022, “Why Swing‐State Voting Is Not Effective Altruism,” the Journal of Political Philosophy ( https://philpapers.org/rec/BREWSV-3 )

I made the below refinements, that don’t make a big difference overall:

Refinement for median day change:

On a median day between 2004 and 2020, the stock market has an absolute value change of 0.49%. Let’s remove that amount from each bar, so that we see the change that could plausibly be attributed to the election result:

One other thing we could try to do is adjust for the amount of surprise which markets registered at the result of each election. Here are the probabilities each candidate had going into the election, per election betting markets:

You can see that prediction markets correctly predicted every outcome except Trump’s 2016 win, to which they gave a 20% probability.

Only one outcome was virtually certain beforehand: Bettors gave Obama a 90% chance of winning in 2008.

This gives us a sense of how much candidates were already “priced in” to the stock market. For example, since markets thought Trump had a 20% chance in 2016, and election day revealed it be 100%, the change in market values should contain 80% of the value of Trump’s Presidency (compared to a Clinton one.)

if we attribute the entire excess change in the stock market to the outcome of the election the day, we get:

I left Obama 2008 out of this graph, because the result is too large, and implausible, because the market’s update on his chances was so small (10%) that the big fall on the day following couldn’t have been due to that. If it were due to his election, then, it’d imply that his election cost the US about half of its future economic potential.)

So, here, I’ll ignore the 2008 datapoint by looking at the median impact of a Presidential election, rather than the average.

After adjusting for that, the median change was from the 2020 election, where Biden’s 20% increase in odds from election night appeared to be worth about 1.71% of the stock market, indicating that his election as a whole was worth about 6.57%.

The lowest-impact election was 2016, in which Trump’s win over Clinton was valued at 1.39% of the market.

So that suggests that the value of a vote ranges from 1.39% to 6.57% of the S&P 500.

In 2024, with the S&P worth $55 trillion, that works out to $767 billion – 3.61 trillion.

I didn’t find good governor data for this cycle, so I’m using the numbers from the last election: https://www.wisdc.org/news/press-releases/139-press-release-2023/7281-2022-governor-s-race-cost-record-164m

I use Silver’s estimates, because his model has been good in the past, and because he’s the only one besides 538 who estimates this. I find some of his results surprising (are New Mexico, Mississippi, and Alaska really as valuable as he thinks?) but 538 actually has pretty similar estimates for those states, so — I guess the data is trying to tell us something.

The study has a pretty complex design, and could use replication. Specifically, Kahan gave subjects a short math intelligence test, and then asked them if the test was valid for measuring open-mindedness. But, before asking if the test was valid for that, the experimenter informed subjects that either side of the climate change debate had scored as the “open-minded” ones. The study revealed that smarter people (who did better on the test) were significantly more likely to change their opinion about the test based on whether the test marked their ideological opponents as more open-minded. That’s one very narrow study — it’d be good to see it replicated more broadly.

My dc vote is worth $0 !

Why isn't there a vote for "Not an American citizen"? :)

Otherwise, great article.